The Price of Restaking

Restaking is one of the hottest narratives in 2024 - ever since EigenLayer introduced the concept of restaking; it caught the attention of the market and amassed more than 1bn dollars in total value locked within months. The market generally believed EigenLayer would present one of the most lucrative “airdrop farming” opportunities of the year - but how should we think about valuing EigenLayer?

This article is not a deep dive into EigenLayer’s infrastructure and technology since this has been widely covered by many venture analysts - but instead I would like to share some thoughts when it comes to valuing EigenLayer given how EigenLayer is one of its kind.

EigenLayer v.s. Lido Finance

EigenLayer invented the concept of “restaking” which enables the use of ETH on the consensus layer to extend crypto economic security to other applications built on top of the smart contract layer. Users could opt in to “restake” their native ETH or liquid staked ETH to secure additional applications for yields as rewards.

EigenLayer’s business model is straightforward - the platform takes a cut from the yield generated by applications built on top of the smart contract layer or what they call “actively validated services”. AVS could be anything from oracles, sequencer networks to even rollups.

The business model is very similar to Lido Finance, the leading liquid staking protocol as in both protocols generate revenue by taking a cut from the yield generated. The major difference is that Lido takes a cut from the native yield generated by the ETH deposited to the platform; while EigenLayer captures yield generated by the additional services built on top of them.

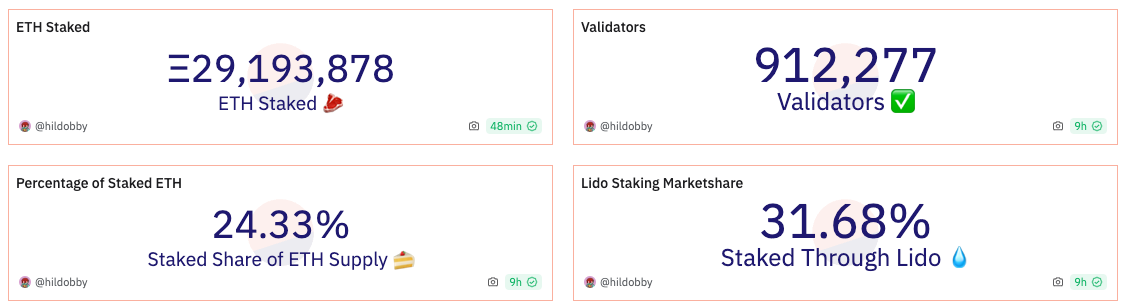

Let’s look at some numbers to quantify the context - Lido Finance currently generates an annualized top line fee of close to 90mn from the total TVL of more than 20bn. Lido is currently trading at close to an FDV of 3bn and this translates to a fee multiple of more than 30x.

Apparently the market trades in expectation and it is unfair to directly come up with a fair valuation with EigenLayer’s current traction even with more than 1bn in total value locked. That being said; this mental model is optically logical because the fair valuation of EigenLayer would linearly scale with the # of applications built on top of the smart contract layer; and presumably these AVS would share revenue with EigenLayer through gas fees.

However, I thought there are 2 key differences between EigenLayer and Lido Finance which might make this mental model less reliable. Firstly, Lido’s cash flow generation ability would linearly scale with the amount of ETH it gathers; but EigenLayer would not. It requires multiple applications to be built on EigenLayer for the smart contract layer to be positive cash flow generating. This demand side driven dynamic might be the major hindrance to profitability while Lido is a supply driven business which is incredibly profitable only by gathering assets.

The next question to this valuation framework is whether or not slapping the same fee multiple of Lido Finance on EigenLayer makes sense. Fee multiple represents the dollar value investors are willing to pay for each dollar in top line fees the application is generating; and as a natural extension it entails the market expectation on the protocol’s growth profile.

Therefore one could argue Lido and EigenLayer should not have the same fee multiple because the growth profile for both applications is entirely different.

The total addressable market of Lido Finance is broadly defined as the total amount of staked ETH; and has a limited growth profile if we benchmark other Proof of Stake networks, not to mention those liquid staked will only be a subset of the total staked amount. Lido Finance also faces immense competition from other liquid staking protocols such as Rocket Pool and some of those are even more restaking aligned.

On the other hand the total addressable market of EigenLayer is relatively undefined; and theoretically speaking the demand could be uncapped because there could be infinite applications that are looking to source security from EigenLayer.

EigenLayer v.s. Celestia

Celestia is another frequently mentioned market comparable to EigenLayer. I thought this might somehow be misled by EigenLayer’s first actively validated service EigenDA which is effectively also a data availability solution. That being said, I do see there being some similarities between what Celestia and EigenLayer are offering.

EigenDA is fundamentally different from Celestia as they adopt DA scaling instead of DA sampling. DA scaling is a method that leverages a complicated cryptographic method called “erasure coding”. This method reduces the number of drives required to continue functioning properly and store all data while maintaining an acceptable level of resilience. EigenDA is not offering any form of consensus and settlement; but instead it only does data attestation.

Celestia does DA sampling instead. Each DA node in the Celestia network still has to store all data which makes them computationally heavy. Celestia therefore added a network of light nodes called the Halo Network to prove that each DA node is still holding the data. If DA nodes fail to prove they have the data, their stake of $TIA tokens would be slashed. After all, Celestia is a full blown blockchain.

If we think about what Celestia is actually offering - they are selling to rollups a consensus layer that comes with cheaper data availability costs such that they are incentivised to build on top of the network. Celestia would therefore accrue value from the demand of security to secure the collective asset value in its ecosystem.

DA nodes have to make sure they store all the required data within this ecosystem; and otherwise they would be slashed. In other words, one could argue that Celestia is ultimately running a business that “sells” and “profit from” security denominated by crypto economic value to rollups.

EigenLayer is essentially also selling “security” and by security I mean when something malicious happens some crypto economic value would be forgone. As aforementioned liquid staked ETH could be restaked to extend crypto economic security to applications on the network; and stakers are exposing themselves to additional “slashing” risks. Applications or AVS are effectively outsourcing the crypto economic heavy part to restaked ETH sourced from EigenLayer.

There are for sure some major differences between what EigenLayer and Celestia is fundamentally offering; but essentially both protocols are profiting or accruing value from crypto economic value. There are still some open questions or fundamental difference in this mental framework structure that could affect the fair valuation.

First of all it is the difference of where does the “security” come from. Celestia bootstraps its own validator set and pays validators through native token inflation to “secure” the network and offer consensus; while EigenLayer sources “pooled security” from restakers who are happy to take on more slashing risks.

Secondly it is who will be responsible when something goes south. As aforementioned EigenLayer’s restakers would take on more risks and their “stake” denominated in ETH would be slashed when a custom condition is met. For Celestia this is more straightforward since DA nodes will have their stake slashed if they fail to offer the required proof. Therefore one could argue EigenLayer’s tokens should not accrue that much value compared to Celestia if there is one in the future.

Closing Thoughts

I like to think that EigenLayer should be priced closer to Celestia than to Lido Finance despite all the similarities in their business and revenue model. Meanwhile I also thought the crypto market is still too nascent to properly attach a price tag to the demand of “security” which is in my opinion worths a lot of money in crypto.

While we thought Celestia rallying from $2 upon launch to the current level of $17 as a relatively unexplained price action; we tend to neglect the fact that the Celestia ecosystem has already seen mature growth with rollups actually adopting their technology such as Manta Network. This is also how Celestia started to accrue more value through the demand of “security”.

Although EigenLayer is not “selling” security bootstrapped by the network itself; the fact that they managed to commoditise the product and commercialise by selling to applications in need deserved to be traded at a premium. I would be very interested to see how the market price their tokens if they finally decided to launch one.

Good reads. Agree on in the near term, the growth trajectory of EL is tightly tethered to the demand side market, making it more akin to TIA than LDO. However, in the long term, I think EL emerges as a more compelling 'Ethereum Align' target, surpassing both LDO and TIA. EL plays a pivotal role in scaling and upgrading Ethereum in two critical dimensions: network and asset.

First, Ethereum as a network is undergoing a significant paradigm shift characterized by modularity. Over the next 6-24 months, I anticipate the introduction of numerous middlewares (DA/Sequencers/L2 stacks), contributing to Ethereum network's performance but simultaneously raising concerns about fragility due to the buckets effect on security.

Second, Ethereum as an asset is losing some appeal with decreasing staking APR. Using the ~60% average staking ratio for PoS chains as a benchmark, I expect Ethereum's staking ratio rising from the current ~25% to 35-40% in the next 12-24 months, resulting in a less attractive staking APR of < 2.5%. With the increases of risk appetite and a ~10% marketwise APR as we enter a bull market, I expect a considerable migration of ETH holders towards alts.

For ETH to moon this cycle, it is important that the above two challenges be addressed properly (whether in-protocol or not), for which EL offers an elegant solution. IMO, EL stands out as the best ETH beta play compared to LDO and TIA, not to mention the substantial growth and premium it stands to gain upon the implementation of its infrastructure roadmap.